Circle’s USDC added roughly $2 billion in supply during the first quarter of 2026, pulling ahead of rival Tether at a moment when the broader crypto market was contracting. It marked the sharpest divergence between the two largest stablecoin issuers since the bear market of mid-2022.

USDC Gains As Tether Loses Ground

While USDC grew, Tether’s USDT shed approximately $3 billion over the same period. Reports indicate USDC has been gaining traction in trading and on-chain transactions, with transfer activity hitting a record high in February. The shift aligns with growing institutional preference for a US-regulated issuer as Congress moves closer to passing stablecoin legislation.

Total stablecoin supply reached $315 billion by the end of March, up about $8 billion from the prior quarter, according to CEX.io data. Growth was slower than at any point since late 2023, but it was still growth — at a time when most other corners of the crypto market were shrinking.

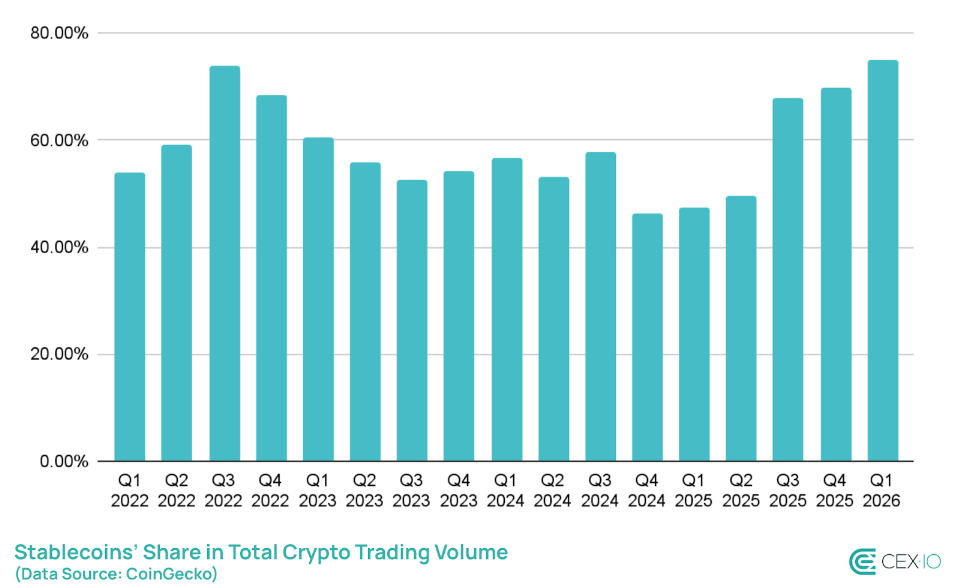

Stablecoins also captured 75% of all crypto trading volume in Q1, the highest share ever recorded. Data shows investors rotated into dollar-pegged assets as a defensive move, choosing to stay inside the crypto ecosystem rather than exit it entirely.

Total stablecoin transaction volume for the quarter topped $28 trillion, extending a run that has seen stablecoins process more value annually than Visa and Mastercard combined.

Yield-Bearing Products Fuel New Supply

A significant portion of fresh issuance came not from USDC or USDT, but from yield-bearing stablecoins — products that pay returns similar to interest-bearing accounts.

That segment is now valued at around $3.7 billion, with daily trading volumes exceeding $100 million, based on CoinGecko data.

The growth has drawn pushback from traditional banks, which have been lobbying Congress against stablecoins that offer returns, arguing they function more like financial instruments than payment tools.

The debate is unresolved, and its outcome could determine how much room yield-bearing products have to grow inside the US market.

Retail Activity Drops As Automated Trading Rises

Not all of the quarter’s numbers pointed upward. Retail-sized transfers — those associated with individual users — fell 16%, the steepest single-quarter decline on record.

Automated trading and algorithmic activity filled much of that gap, accounting for approximately 75% of all stablecoin transaction volume during the period.

CEX.io’s report frames the overall picture as one of structural growth under pressure — a market where institutional and automated flows are increasingly driving the numbers, even as everyday participation fades.

Featured image from Meta, chart from TradingView

{kind=link}